Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

The audited accounts of different commercial banks for 2019 started coming out in the newspapers in recent weeks. Usually, these are published earlier in the year during April-May. Dislocations related to Covid-19 pandemic may have caused this inadvertent delay.

The year 2019 marked a transitional period for the banking sector in Bangladesh following major policy interventions in 2018. In June 2018, the association of private sector banks ABB made the public commitment of bringing down the deposit interest rate to 6.0 per cent and lending interest rate to 9.0 per cent, and extracted important concessions from the government in the form of (a) 1.0 per cent lower Cash Reserve Requirement (CRR); (b) extension of time limit to roll back AD ratio within the reduced Bangladesh Bank ceiling; (c) lower corporate tax for banks; and (d) provision of increased government deposits in private banks.

The State-Owned Commercial Banks (SOCBs) followed suit by making the announcement in July 2018 of bringing down interest rate within single-digit level. Since then, barring small aberrations, the SOCBs implemented these decisions quite earnestly throughout the remaining months of 2018 and the whole year of 2019. In contrast, the private sector banks did not comply with their commitment creating differential interest rates regime amongst the state-owned and private sector banks.

How have the SOCBs fared in the face of such uneven competition? The recently published audited accounts for 2019 provide an opportunity to gauge the impact on the financial performance of these banks arising out of the uneven playing field.

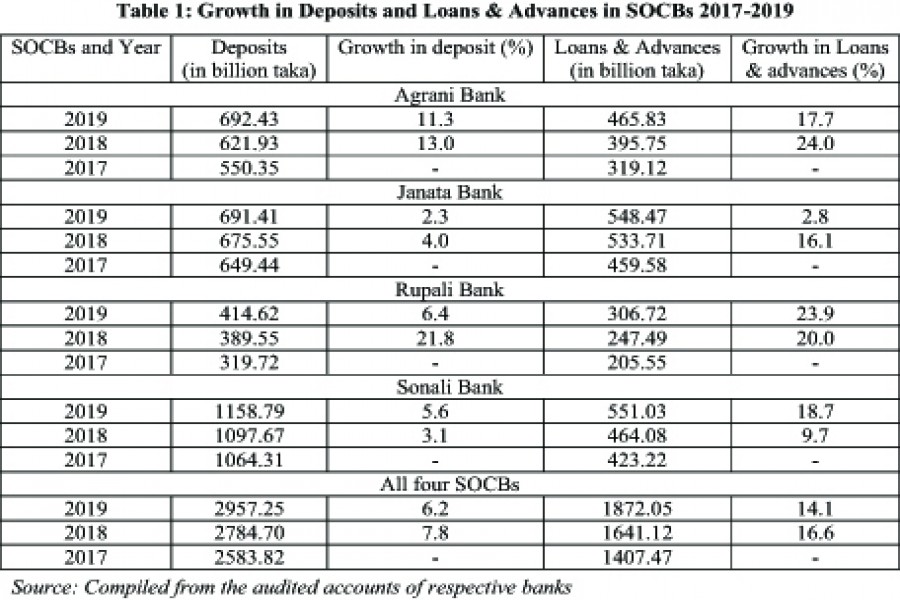

GROWTH IN DEPOSITS: Table-1 presents information on growth of deposits in four major SOCBs during 2017-2019. As is evident from the table, the adverse impact on growth of deposits in the SOCBs has not been very significant. All four SOCBs experienced positive growth in the deposits, albeit, at a varying degree. The average rate of growth of deposit for the four SOCBs together declined marginally from 7.80 per cent in 2018 to 6.20 per cent in 2019.

Bangladesh Bank data shows that deposit growth in the banking sector as a whole during 2019 was 12.60 per cent. Against that benchmark, the deposit growth of 6.20 per cent for the SOCBs is somewhat low, although one of the SOCBs, namely, Agrani Bank, experienced respectable growth of 11.30 per cent in deposits during the same period.

Evidence suggests that notwithstanding alluring away of some deposits from the SOCBs by the higher deposit interest rate offered by the private banks, the confidence of the general public in the security of their deposits in the SOCBs helped keep such displacement of SOCB deposit at a tolerable level. Recent scams relating to private banks, particularly the crisis centring Farmer's Bank, may have contributed to the greater sense of trust towards the SOCBs.

LOANS AND ADVANCES: According to Bangladesh Bank data, growth of credit to the private sector during 2018 was 13.30 per cent, which fell to 9.80 per cent during 2019. As can be seen from Table-1, the SOCBs experienced significantly higher growth in loans & advances in both these years.

LOANS AND ADVANCES: According to Bangladesh Bank data, growth of credit to the private sector during 2018 was 13.30 per cent, which fell to 9.80 per cent during 2019. As can be seen from Table-1, the SOCBs experienced significantly higher growth in loans & advances in both these years.

As would be expected, with lower lending interest rates the SOCBs were faced with more demand for credit in 2019 and evidently, except Janata Bank, the other three SOCBs did lend out at a much higher rate than overall growth of credit to the private sector.

As we are aware, the government move to put a ceiling on the lending interest rate has encountered widespread criticism in recent times mainly on the ground that it will discourage banks from lending and will adversely affect credit flow to the private sector. Recent declines in credit growth to the private sector is interpreted as a reflection of that apprehension coming true.

The evidence presented in Table-1, however, clearly shows a differential response pattern between private banks and SOCBs with respect to growth in lending. While private banks have put a brake on their lending drive, the SOCBs are absorbing some of the excess credit demand by drawing down their underutilised lending capacity. This also got reflected in the rising AD ratio of all four SOCBs during 2017-2019 (Fig.1).

NET INTEREST INCOME: The SOCBs not only adhered to the ceiling on lending interest rate during 2019, unlike the private banks, they also abided by the Bangladesh Bank guideline regarding interest rate spread. Also, in the face of uneven competition from private banks, the deposit interest rate they were forced to offer caused the interest rate spread to get squeezed causing adverse impact on their net interest income.

Notwithstanding such unfavourable situation, Agrani Bank posted a respectable level of Tk 6.33 billion (633.0 crore) net interest income during 2019, which was nearly 29.0 per cent lower than Tk 8.92 billion net interest income earned in 2018 (Table-2). Similarly, Janata Bank reported Tk 4.54 billion earned as net interest income in 2019, 40.0 per cent lower than Tk 7.52 billion net interest income earned in 2018. Rupali Bank suffered a staggering 99.0 per cent decline in their net interest income while Sonali Bank managed to reduce their negative interest income level somewhat. Overall, the four SOCBs earned a total net interest income of Tk 6.77 billion, though nearly 47.0 per cent lower than the 2018 level.

OPERATING PROFIT, CLASSIFIED LOANS AND NET PROFIT: Agrani Bank was the only SOCB experiencing positive growth in operating profit (8.20 per cent) during 2019 (Table-3). Agrani Bank also earned the second highest level of operating profit (Tk 9.0 billion) next to Sonali Bank (Tk 17.10 billion) during 2019. But Sonali Bank had an AD ratio of only 47.60 per cent against 67.30 per cent in the case of Agrani Bank. The operating profit of Janata and Rupali Banks were Tk 7.09 billion and Tk 1.93 billion respectively. For the four SOCBs together, the level of operating profit was Tk 35.12 billion in 2019, which is 15.30 per cent less than the previous year.

An important policy intervention of 2019 was made through the Bangladesh Bank Circular BRPD-5, which allowed those who were not wilful defaulters to reschedule their loan for a period up to 10 years with only 2.0 per cent down payment with scope for waiver of unapplied interest and interest accrued in the suspense account. All four SOCBs availed this circular, which helped them bring down the proportion of their classified loans. Agrani Bank ended up with the lowest proportion of classified loan (14.26 per cent) followed by Rupali Bank (15.05 per cent), Sonali Bank (20.32 per cent) and Janata Bank (26.62 per cent). For all four SOCBs, the proportion of classified loan came down from 25.40 per cent in 2018 to 19.80 per cent in 2019. Reductions in classified loan helped net profit of the four SOCBs to increase by 16.50 per cent in 2019 over 2018.

To sum up, the evidence presented above shows that the impact of unilateral implementation, since mid-2018, of the single digit lending rate of interest by the SOCBs on their financial performance has been rather mixed.

First, the apprehension that such a ceiling on the lending interest rate will have a serious adverse impact on the growth in deposit, and loans & advances, does not seem to have been borne out. The growth in deposit for the four SOCBs taken together declined marginally from 7.80 per cent in 2018 to 6.20 per cent in 2019. One of the SOCBs, namely, Agrani Bank, posted 11.30 per cent growth in deposit, which was close to the 12.90 per cent growth for the overall banking sector in 2019. Similarly, all the SOCBs except Janata Bank experienced impressive double-digit growth in loans and advances, with the combined growth in the level of loans and advances of these four SOCBs working out at 14.10 per cent, marginally lower than 16.60 per cent recorded in 2018. In contrast, the overall growth of credit to the private sector declined significantly from 13.30 per cent in 2018 to 9.80 per cent in 2019. The rising AD ratio of all four SOCBs during 2019 further corroborated this performance with regard to growth in loans & advances.

Second, as would be expected, the lower lending interest rate and maintenance of interest rate spread as per Bangladesh Bank guideline, implied lower net interest income for these banks. The four SOCBs together experienced nearly 46.60 per cent decline in their net interest income. But once again, Agrani Bank was better able to absorb the shock, with its net interest income declining by 29.0 per cent. Agrani Bank posted a net interest income of 6.33 billion taka in 2019 against 6.77 billion taka recorded for the four SOCBs taken together,

Third, as would be expected, the declining interest income contributed towards declining operating profit in 2019. For the four SOCBs taken together, operating profit declined by nearly 15.30 per cent. But here again, Agrani Bank was the exception being the only SOCB posting positive growth (8.20 per cent) in 2019. This implies that with right treasury management and optimal investment portfolio mix it is possible to achieve positive growth in operating profit even under situation of declining net interest income.

Fourth, taking advantage of the Bangladesh Bank circular BRPD-5, allowing flexible condition for loan rescheduling, the four SOCBs succeeded in bringing down the proportion of classified loans from 25.40 per cent in 2018 to 19.80 per cent in 2019. Agrani Bank had the lowest classified loan proportion of 14.30 per cent in 2019 followed by Rupali bank (15.05 per cent), Sonali Bank (20.32 per cent) and Janata Bank (22.62 per cent).

Finally, the reduced classified loan helped the SOCBs to experience increase in their net profit as provision requirement declined. The four SOCBs together showed 16.80 per cent growth in net profit, the main contribution coming from Sonali and Agrani Bank with net profit of these two banks recorded at the levels of Tk 2.71 billion and Tk 1.07 billion respectably.

How long-lasting are these gains of the SOCBs will depend on the effectiveness with which they monitor the rescheduled loans and ensure regular payments of instalments under the rescheduling deal. The fact that the attractive level of interest waiver granted under BRPD-5 dispensation becomes effective only after full repayment has been completed will, hopefully, act as an important carrot in this somewhat controversial rescheduling facility rolled out by Bangladesh Bank.

Dr Zaid Bakht is Chairman, Agrani Bank Ltd. zaidbakht@gmail.com