Subsidy issues and the budget for FY23

Fahmida Khatun, Mustafizur Rahman, Khondaker Golam Moazzem and Towfiqul Islam Khan

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

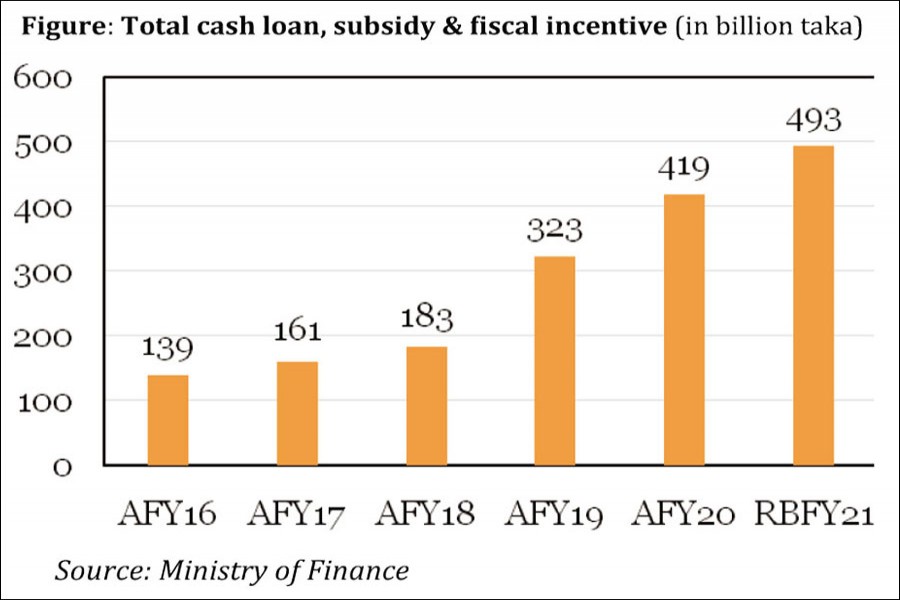

The subsidy management has emerged as a challenging area from the perspective of the broader fiscal management as Bangladesh embarks on the post-Covid 19 recovery phase. Subsidy, as is known, is provided in many forms: cash loan support and fiscal incentives to different sectors including agriculture, export, jute goods, power and energy. Over the years, the total subsidy budget has been on the rise, from Tk 139.24 billion in FY16 to Tk 493.30 billion in FY21 - an increase of 50.8 per cent per year. The highest amount is spent on fiscal incentives served to different sectors (56.2 per cent in FY21), followed by cash loans for BPDB, BPC and BJMC (30.4 per cent) and subsidies for food and gas & others (13.3 per cent in FY21).

The allocated amount of subsidy in revised budget of FY21 was 1.64 per cent of the Gross Domestic Product (GDP), while the total actual expenditures on the same were 1.27 per cent and 1.53 per cent of GDP in FY18 and FY19, respectively. The increase in the total subsidy expenses is attributable to an increase in fiscal incentives (from 0.46 per cent in actual budget in FY19 to 0.92 per cent of GDP in revised budget of FY21); thanks to a significant increase in incentives for the jute goods and the recent introduction of cash incentives on inward remittance flows. Likewise, the food subsidy expenses have increased significantly (by more than four times) since FY19. On the other hand, the major part of cash loan support (75 per cent of the total cash loan since FY2014) has been allocated to the BPDB, a government agency. However, in the backdrop of the highly significant liabilities in the power and energy sector (Tk. 432.14 billion in FY22) - mainly due to the rise in petroleum and LNG prices -, the allocation for cash loan support to this sector could experience a steep increase in coming days.

Various studies have questioned the extent to which the various subsidies have actually been effective in terms of actual contributions, particularly in addressing the prevailing market failure and improving equity in targeted sectors and economic activities. The proposed budget for FY23 should highlight the rationalisation of subsidy and subsidy management from medium to long-term perspectives.

Following recommendations may be considered as regards subsidy allocation in the FY2023:

PRIORITISE PAYMENT OF HIGHER SUBSIDY FOR FERTILISER: Allocation of subsidy for the agriculture sector needs to be increased, particularly for accommodating the higher import price of fertiliser. International fertiliser price has experienced a record rise in recent months due to Covid 19 restriction, temporary banning of fertiliser export by China (to meet its domestic demand), banning of fertiliser export by Russia (due to the ongoing Russia-Ukraine war) and higher raw material costs, mainly of gas. An additional subsidy amount of Tk 185.0 billion would be needed to be allocated in FY23 budget in view of price rise if the subsided fertiliser price for the farmers is to be kept at the present level. It is to be noted that various forecasts indicate that the international price of fertiliser is likely to remain higher at least till the end of 2023, which implies that this higher subsidy against the higher price may need to be continued in subsequent years as well. Budget for FY23 should be informed by the current and anticipated fertiliser price in the global market.

STRENGTHEN MARKET MONITORING TO ENSURE ACCESS TO INPUTS AT SUBSIDISED PRICE: It was reported that farmers had to buy fertiliser at a higher than the stipulated subsidised price; same was seen for other subsidised agro-inputs. Weak market monitoring, particularly at retailers' and distributors' ends, is perhaps the reason for this situation. Ministry of Agriculture should be asked to strengthen monitoring of the supply channel, from dealers and distributors to farmers, to ensure efficient distribution of fertiliser and other inputs.

MAINTAIN THE CURRENT LEVEL OF SUBSIDY ON INWARD REMITTANCES: The recent 0.5 per cent increase (in January 2022) in direct incentives on remittance flows in addition to earlier 2 per cent (in total 2.5 per cent) have contributed positively in the form of remittance flows to Bangladesh. This has benefitted remittance-receiving households through increased purchasing capacity amid high inflationary pressure. Given the rising fiscal expenditure owing to the rise in cash incentives, the government should prioritise curbing the migration cost and lowering the remittance sending cost from selected countries. At present, there is a significant gap between the rate for remittance kerb market rate. CPD had earlier advocated of gradual depreciation of Taka. However, in view of the current high commodity price, exchange rate stability should be given priority and other measures to encourage transfer of remittance through the official channels should be emphasised.

ALLOCATE MORE RESOURCES FOR FOOD SUBSIDY: Given the significantly high level of agricultural commodity prices in the world market and high domestic inflationary pressure, subsidised food distribution among the targeted group of people needs to be increased in the next fiscal year. Hence, the allocations for food subsidy, through direct in-kind support and price support, need to be increased.

RESTRUCTURE SUBSIDY IN VIEW OF LDC GRADUATION: LDC graduation will mean that certain forms of industrial and export subsidies will be WTO-incompatible. Accordingly, for example, the direct export subsidy allocation, such as cash incentives to major export-oriented sectors, will need to be gradually reduced. Bangladesh should consider innovative incentive schemes similar to the ones in India, China, and Vietnam to support the export industry. For example, India provides incentives for manufacturing investment and Vietnam and China for skill and technology upgrading. At the same time, government should design a mid-term strategy to decide to what extent such subsidies will be fiscally sustainable. Instead of subsidising in the form of cash incentives and tax concessions, the government should consider providing in-kind benefits (such as active labour market programmes, social safety net programmes, health insurance and support for ease of doing business).

UNDERTAKE COMPREHENSIVE REFORMS OF THE SOES: A large part of SoEs has been a continuous drag on the economy for the past years. Only in FY19, the net loss of four SoEs, BCIC, BTMC, BSFIC, and BJMC, reached Tk 24.16 billion. Government should undertake a comprehensive review of SoEs, consider liquidation of losing SoEs and handing over of SoEs assets to the SEZ and EPZs for the development of special economic zones for SMEs and other industries.

RENEGOTIATE CONTRACTUAL ARRANGEMENTS FOR PAYING CAPACITY PAYMENT TO INDEPENDENT POWER PRODUCERS: Excessive electricity capacity payment is causing a huge expenditure burden on the government agency, the BPDB. Consequently, BPDB has been saddled with significant losses (Tk 43.52 billion in FY20; Tk 86.64 billion in FY21). In order to reduce the subsidy pressure in the power sector, government should instruct the Ministry of Power Energy and Mineral Resources (MoPEMR) to renegotiate the contracts as regards capacity payment negotiated earlier with the independent power producers. The GoB should instruct the MoPEMR not to sign any new contracts or renew contract in the power sector with provisions for capacity payment.

GRADUALLY PHASE OUT FOSSIL-FUEL BASED ENERGY: According to recent media reports, BPDB and BPC have been incurring a loss of Tk 240 million and Tk 630 million per day, respectively, in view of increased global energy prices (UNB, 2022). The power and energy sectors will need to be provided significant subsidies in FY23 as short-term measure so that the loss incurred by power and energy sector is not passed on to consumers and producers. Government may consider withdrawing VAT and other duties at the import stage to lessen the import price of petroleum and LNG. Government could think of borrowing short term loans from multilateral agencies (IDB, World Bank) or bilateral sources (KSA, Qatar) to pay the import bill for energy (i.e., petroleum). In the medium to long term government should put focus on exploring natural gas by exploring off-shore and on-shore potential sources. Adequate resources should be allocated in FY23 budget towards this. The budget should have provisions for subsidising and incentivising investment in renewable energy-based power generation.

Dr Fahmida Khatun is Executive Director, Centre for Policy Dialogue (CPD); Professor Mustafizur Rahman is Distinguished Fellow, CPD; Dr Khondaker Golam Moazzem is Research Director, CPD; and Mr Towfiqul Islam Khan is Senior Research Fellow, CPD. towfiq@cpd.org.bd; avra.bhattacharjee@gmail.com