Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

It is now a widely considered view that the global influence of the US may be declining, potentially leading to a period where no single country holds superpower status. There are many factors that are cited to provide support to this hypothesis which include changing global economic and political dynamics, the exigencies of the global system, and the rise of more powerful competitors in Asia and Europe. The relative decline of the US is attributed to high public debt and other fiscal issues, slow economic growth, rising income inequality, corporate interests and the imperial overreach.

To put it more precisely, the considered view is that both the "American century" and the "unipolar moment" of the US in history will have come to an end where the US will likely become one among other equals or at best primus inter pares among other equals.

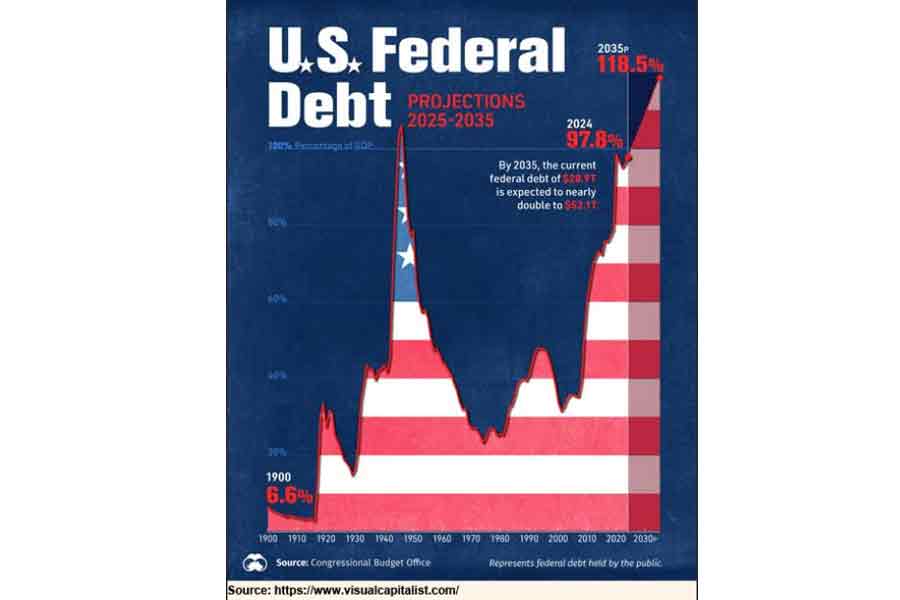

A report published by the Brookings Institution recently outlined how rising US federal debt now standing at US$36 trillion could spark a very serious financial crisis in the US and the world. While the chances of such a crisis remains low, the report, however, suggests that a financial crisis will likely to be through the repurchase or the repo market. This is the market where financial institutions obtain their short-term credit.

Now President Donald Trump's "big, beautiful bill' further extending tax cuts for corporations and the wealthy has passed through the Congress. The Congressional Budget Office (CBO) estimated that this bill would add more than US$3 trillion to the deficit. This has sparked fears in financial markets that the US is on the road to a debt crisis.

In fact, concerns over the rising levels of debt in the US even before the "big, beautiful bill" was pushed through. Moody's decision to cut the credit rating (A to Aa1) for the US from its top grade on May 16, now means that the US no longer enjoys the top rating from any of the three (other two being Fitch and S&P who also have downgraded the rating for the US) major rating agencies. This is the first time that this has happened in history. Of the 200 countries around the world, only 10 plus and the EU are rated as risk-free by all three major credit agencies and the US is not among them and does not enjoy the AAA rating now.

Many are dismissive of risks of large debts and deficits because the US as the world's strongest economy need not fear investors fleeing from its debt and the dollar. However, now there is less basis to be confident about this point in the current political and economic climate in the US.

Appearing on a television programme on June 1, US Treasury Secretary Scott Bessent was forced to go on public to say that the US will not default on its loan payment. This is a further indication that there are some fundamental problems in the system of which he in charge.

Federal or sovereign debt is the total amount of money the US government owes to lenders both at home and abroad. That debt now amounts to US$36.2 trillion representing 122.6 per cent of the country's GDP relative to 34.5 per cent in 1980 and is continuing to grow. That is about US$106,000 for every citizen of the country. The annualised cost of servicing this debt was US$726 billion in July 2023, which accounted for 14 per cent of the total federal spending in that year. The share of federal debt held by foreigners has declined in recent years. In December 2024, foreigners held 30 per cent of the publicly held debt compared to 50 per cent in 2014. Interest on the debt paid to foreigners in 2024 was $230.6 billion. The interest payment bill is now emerging as the single largest item in the UD federal budget amounting close to $1 trillion.

The US government borrows money by selling Treasury bonds, or simply Treasuries. Buyers of Treasuries are banks, pension funds and foreign governments and they in return receive interest payments which is called the Yield. There exists a negative relationship between the interest rate and the bond price. This is because if investors start selling the existing bonds, the price drops, and the government then must raise the interest rate (yield) to sell newly issued bonds. Therefore, a fiscal crisis could arise when there is a sudden downturn in demand for Treasuries relative to supply and that could trigger a sharp and persistent spike in interest rates.

The US has the highest amount of debt in the world. In terms of debt/GDP ratio, the US is one of the 10 most-indebted countries in the world but not at the top of the table.

The US federal borrowing is necessitated by the federal budget deficit. The federal budget deficit arises when the government spends more than it collects in revenue during the fiscal year.

Now if the intractable balance of trade deficit which amounted to US$131.4 billion in 2024 is added, that would represent about 3.5 per cent of GDP. In this case this deficit arose out of US consumers consuming more than they produced or more precisely the deficit is only really determined by the gap between savings and investment. But the strong performance of the US economy, in other words, lies behind the rise in the US trade deficit.

Over the past eight decades, the status of the US as an economic and geopolitical superpower and the role of the US dollar as the world's dominant currency have reinforced each other. As these two facets of US power have reinforced each other it can be argued that a decline in either of them could trigger a downward trend in US influence around the world.

The US' relative economic prosperity has been largely guaranteed by its currency because the US dollar is accepted as global moneyin financial transactions between countries around the world. The strength of the US dollar lies in its economic strength and dynamism. Rising productivity enabled the US to become a very competitive economy and a stable and predictable political environment further added to ensure a highly prosperous and stable economy. All these along with institutional integrity, rule of law and the independence of the central bank also added to the currency's attraction as a reserve currency.

Also, its geopolitical clout further added to the dollar's attraction. Now it is still the leading reserve currency in the world despite the Euro, Yen, Yuan and Swiss Francs are making a steady dent into that market. At the end of 2024, the dollar accounted for 58 per cent of global foreign exchange reserves, while 10 years earlier that share was 65 percent. While the US dollar continues to cede ground to nontraditional currencies in global foreign exchange reserves, but it remains the preeminent reserve currency.

In fact, the Bretton Woods Agreement of 1944 established the post-war international monetary system, with the U.S. dollar to become the world's primary reserve currency for international trade, linked to gold. Despite the abandonment of the Bretton Woods system in 1971, the dollar continues to play this role to this day.

However, the dollar's preeminent role in international currency transactions and foreign reserve holdings, has long been associated with the US' exorbitant privilege to finance large fiscal deficits at low interest rates. Also, the US has been able to continue to accumulate sovereign debt because of the dollar's role as the global reserve currency. But now high fiscal deficits could weaken the exorbitant privilege that has enabled the US to sustain large fiscal deficits in the past.

Trump's tariff policy has the potential to weaken the standing of the dollar because that has shaken the confidence of investors in the US economy causing the dollar to depreciate. The prospect of a big increase in the deficits associated with Trump's tax cuts, which led to a ratings downgrade by Moody's could also potentially work against the dollar.So,if the dollar's unique status wane, the US will face the day of reckoning.

As the size of the US economy relative to the rest of the world continues to shrink, this dynamic may begin to be turned on its head. Maintaining a global military presence would be harder to finance in the future if the US dollar were to lose its dominant reserve position precipitating a crisis for the US. Also increasing weaponisation of the dollar is driving many countries to diversify away from the dollar. It is not just the stock market; the dollar is depreciating since Trump took office. Interest rates on long-term government bonds have been rising. Unlike the fall in the stock market, the rise in interest rates will have very real effects on the economy since it will further slowdown economic activity.

muhammad.mahmood47@gmail.com