Who should be given direct livelihood support?

Ahsan Mansur, Abdur Razzaque and Bazlul H Khondker

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Covid-19 has now turned into a major global health and economic crisis unprecedented over the past 100 years since the Spanish flu of 1918. Economic activities across the world have grounded to a dramatic halt. Countries and multilateral agencies (Asian Development Bank, World Bank, International Monetary Fund or IMF, OECD etc.) have started crunching the numbers to assess the likely economic and social costs of this global pandemic. Most recent IMF projections show an overwhelming majority of global economies to contract in 2020 and the growth in the Asia-Pacific region will hit the lowest since the 1960s. Hundreds of millions of people worldwide have lost their jobs and are confronted with survival and livelihood struggles. A study by UNU-WIDER shows that the resultant economic consequences could increase global poverty by as much as half a billion people, or 8.0 per cent of the total human population. This would be the first time in the past 30 years since 1990 that poverty has increased globally. The WFP has also warned that the world may see famines of biblical proportions in 10-39 countries of the world.

Bangladesh has also started dealing with the severe consequences of Covid-19 with curtailed economic activities manifested in factory closures, massive loss of employment, cancellation of export orders, declining remittance inflows, and depressed demand for domestically produced goods and services. The government has now declared that the entire country is at the risk of coronavirus pandemic. Emerging assessments seem to suggest that export earnings in FY20 could be $5.0-$8.0 billion lower than that of the previous year (i.e., up to a negative growth of 20.0 per cent). Remittances that have traditionally played a critical role in boosting consumption demand for rural households were down by 12.0 per cent (in March) and the inflows are likely to deteriorate further in the coming months. Manufacturing activities that have been the engine of Bangladesh's Gross Domestic Product (GDP) growth are also likely to have plunged to an exceptionally low level. The services sector, including hotels & restaurants, construction, transportation, etc., has taken a massive hit by lockdown measures and shrinking demand.

The World Bank projected that overall economic growth in the current (FY20) and next fiscal year (FY21) to be in 2.0-3.0 per cent range. While it is too early to predict economic activities in FY21, the forecast for FY20 is plausible. Even if the government's claim of 8.0 per cent growth in the first eight months of FY20 is accepted, a conservative assessment of a negative growth of (-)9.0 per cent for the remaining period will yield an overall growth 2.25 per cent for the entire fiscal year. Many economic analysts would argue that even prior to the unfolding of Covid-19 crisis, economic performance was very subdued with export earnings in the first eight months of the current fiscal year declining by 5.0 per cent over the corresponding period of the previous year; private sector credit decelerating to 9.0 per cent-- the lowest level in two decades; single-digit government revenue growth pointing to a huge shortfall from its target; and government borrowing from the banking system being a record high. That is, from an already shaky point of departure, the overall economic situation has become even more precarious for Bangladesh.

Notwithstanding the above, the government's declared policy support measures in dealing with the economic fallout of Covid-19 deserves appreciation. With an initial stimulus package of Tk 727.50 billion (2.5 per cent of GDP), further support programmes have been announced subsequently to expand the budgetary allocation to Tk 956.19 billion (3.30 per cent of GDP). The support includes working capital loan fund for manufacturing and service industries, export promotion fund, pre-shipment credit refinancing, a special fund for export-oriented industries, working capital support for cottage, micro, small and medium enterprises, rice procurement budget, working capital support for farmers, agricultural subsidy, and safety net expansion.

The unfolding extraordinary situation inflicted by COVID-19 requires extraordinary measures and as such the policy intent of those support measures is quite clear. Given the institutional capacity and record of governance, effective implementation of the stimulus package will be a matter for future evaluation. At this moment, the following issues should be given careful consideration for immediate policy attention:

(1) Much of the stimulus package is related to economic recovery while at this moment addressing hunger and minimum basic needs constitutes the utmost priority. Millions of poor and vulnerable citizens (including the 'new poor' arising from job losses or forgone income-earning opportunities) are now faced with serious livelihood challenges and thus need support.

(2) Given the transmission patterns of Covid-19 as evident from the experiences of Europe and the United States (US), social distancing and lockdown measures may be required for a protracted period. That is, the economic recovery in any significant way could be months away. Therefore, livelihood support mechanisms for a three to six month period should be an important consideration.

(3) Social distancing measures can only be effective when the people in need have the assurance of direct assistance delivered in a regular manner for as long as it is needed.

(4) We do not say that it is an easy task but designing and implementing a comprehensive support system by directly targeting the poor and vulnerable groups is not impossible either.

Against the backdrop, we emphasise on cash assistance delivered through a digitised system, using the mobile phone-based financial network, to people that would need support. We make our recommendations implementable by working out realistic cost estimates. At the outset, we also acknowledge that it might not be possible to strike a fool-proof programme design. There can be targeting errors, but we propose measures so that such leakages are limited.

It is not easy to estimate the size of population (or, the number of households) that need immediate support to stave off hunger and minimum needs during this crisis. In the absence of a fully-functioning elaborate identification infrastructure (i.e., unemployment insurance number; social security number; comprehensive tax identification number etc.), two possible approaches - income loss and job loss -- could be used to determine the size of the potential beneficiaries. Any method is unlikely to be perfect but the use of available information can provide some usable estimates.

INCOME LOSS APPROACH: A PPRC/BIGD survey (April 17, 2020) finds large income losses among poor and vulnerable population groups. The rapid assessment, conducted between 4 and 12 April 2020, comprising a sample of 5,471 respondents (with 51.0 per cent urban residents and the rest 49.0 per cent from rural areas) shows that income of urban residents fell, on an average, by 82.0 per cent (in comparison with their monthly income in February 2020), while corresponding reduction for rural respondents turns out to be 79.0 per cent. The estimated number of new poor resulting from Covid-19 related economic disruptions is 38.16 million: about 27.0 million in rural areas and 11.0 million in urban areas. Therefore, this new poverty rate is estimated as 22.6 per cent (i.e., 38.16 million as proportion to the total population of 170 million). When the existing 18.90 per cent poor is added to the new poor, the poverty incidence jumps to 41.5 per cent. The survey reveals that only 14.0 per cent of the respondents received some government assistance, while another 4.0 per cent had access to support offered by the NGOs. With their current savings, the rural poor can manage 13 more days' livelihood and the urban poor can sustain just eight days.

Using the 2016 Household Income and Expenditure Survey (HIES), the latest official database for assessing poverty, it can be worked out that a 10.0 per cent reduction in household consumption across-the-board would increase poverty incidence by 9.70 percentage points with the overall headcount poverty rate rising to 34.10 per cent. When consumption declines by 15.0 per cent, the corresponding rise in poverty would be 15.2 percentage points. A further decline in consumption expenditures by 20.0 per cent will make the poverty rate 21.2 percentage points higher (with an aggregate poverty incidence of 45.5 per cent).

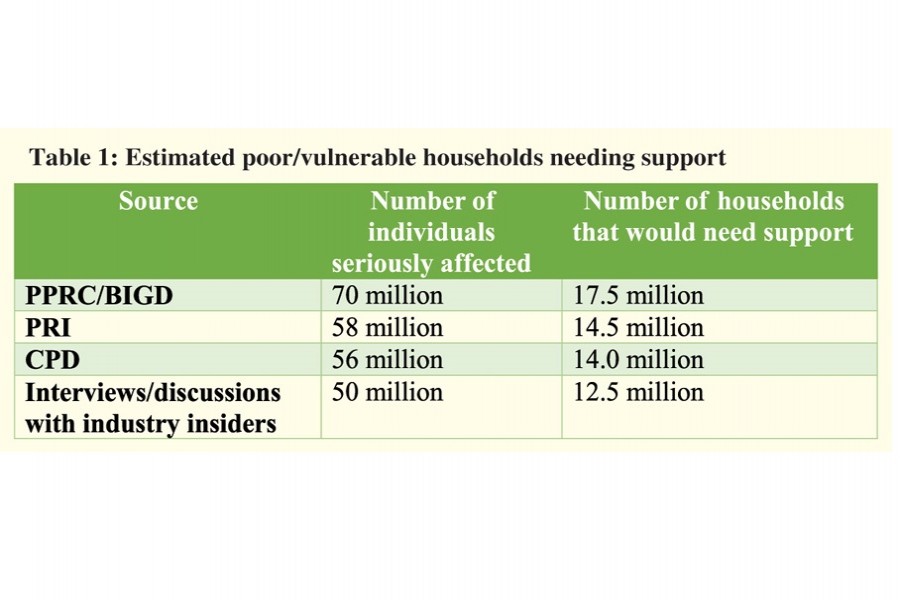

We further estimate that if household incomes are falling in the range 8.0-15.0 per cent, the size of the new poor rises between 12.8 million and 26.0 million with the overall size of poor households reaching 44.50 million and 58.10 million, respectively. Just for comparison, our estimate of 58.10 million is less than the PPRC/BIDG extrapolated 70.0 million. One reason for this difference could be that the PPRC/BIDG survey was targeted towards more poor and vulnerable population groups. Amongst others, the Centre for Policy Dialogue (CPD) proposed that the government should provide cash aid to 11.90 million poor households across the country to help them cope with the ongoing coronavirus crisis and the subsequent adverse implications arising over the next two months (May-June).

EMPLOYMENT LOSS APPROACH: Estimates of job losses are preliminary in nature and are based on the so-called heuristic method. According to many newspaper reports, millions of people, mainly engaged in the informal sector, have become jobless. A telephone-based survey undertaken by a newspaper shows that as high as 47.0 per cent of readymade garment workers have lost their jobs in the backdrop of widespread cancellation of export orders and uncertainty about future export prospects. It has also been reported that millions of transport workers were left without any work after the imposition of the nationwide lockdown. According to various rights groups and labour unions, an estimated 9.0 million workers have had no source of income since the enforcement of lockdown and social distancing measures. Our over-the-phone interviews and discussions with industry insiders during 10-17 April 2020 suggest the loss of employment could have badly hit as many as 10.0-12.0 million households.

Despite varying estimates, it is quite clear that the number of households who would need assistance is within an acceptable range. A simple average of the four estimates (Table-1) would result in 14.60 million households. The government has already announced a specific wage support programme for the RMG workers. If the factory owners are interested to take advantage of the package and strive for paying their employees, which they claim of a size of 4.0 million, these workers' households might not require any further direct cash assistance. There is currently no information on the number of unique households comprising garment workers. However, under plausible assumptions, consideration of unique garment workers' households, could lead to a need for assistance for a lower number of 10.0 million to 12.0 million households. However, it is worth pointing out that the recent crisis has revealed that wage digitisation covers only around 12.0 per cent of garment workers and it is not clear if factory owners, even with the assistance of wage support package, will pay for their all workers when they are away from work.

Dr Ahsan H Mansur, Executive Director, Policy Research Institute of Bangladesh (PRI); ahsanmansur@gmail.com;

Dr Abdur Razzaque, Research Director, PRI; and

Dr Bazlul H Khondker, Director, PRI.

The article is based on PRI's policy brief titled 'Reaching Out to the Poor and Needy with Direct Cash Support: Dealing with the Last-Mile Delivery Challenge', prepared under PRI's Policy Advocacy Initiative on digital financial services in Bangladesh. Research assistance was provided by Azmina Azad and Promito Musharraf Bhuiyan.