Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

General provisioning for normal credit loss in banking is inevitable and also acceptable both from credit risk management as well as accounting perspectives. But specific provisioning seems analogous to the proverb : One doth the scathe, another hath the scorn" ( i.e., one is punished for another's sin). Simply speaking, interest paid by good borrowers is being used in banking as a buffer for adjusting the loan dues from the defaulters. Specific provisions in particular arise as a result of escalating non-performing loan (NPL) beyond a tolerable level ( i.e., maximum 5 per cent may be considered normal). Present discussion aims to examine the rationale behind huge provisioning, and as an alternative paradigm, to focus upon the crucial need to smooth out the legal path to quick and unhindered recovery drive.

International Accounting Standards Board (IASB), Basel Committee on Banking Supervision (BCBS), Financial Accounting Standards Board (FASB) suggest /provide guidelines for provisioning. International Monetary Fund (IMF) & World Bank advocate for provisioning and National Banking Regulators / Central Banks make it mandatory for the banks and financial institutions to comply with loan classification and provisioning guidelines. So far, provisioning has been made following incurred-loss model. The Basel framework, particularly Basel III, requires banks to hold capital for potential credit losses, and it emphasises the use of Expected Credit Loss (ECL) models to ensure adequate provisioning based on forward-looking estimates of losses. Accordingly, our central bank has instructed the banks to prepare for phase-wise implementation of ECL model alongside general provision.

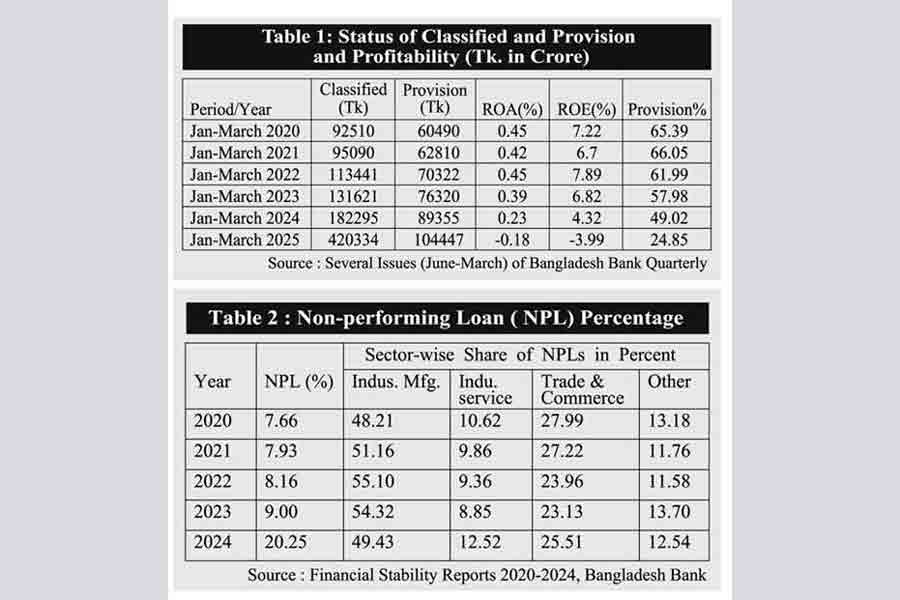

Accounting standard board argues for loan loss provisioning to establish discipline and transperancy in financial reporting whereas banking corporate governance ought to ensure disciplined behaviour of defaulters by resorting to legal measures. Provisioning as suggested and instructed by Basel and national supervisors is just cleaning the financial statements, not containing the risk of credit loss at all. Loan loss provisioning refers to allocating fund from profit to cover potential losses from defaulted loans of banks or other lending institutions. It is claimed that these provisions act as a financial buffer so that banks can absorb losses without severely impacting their overall financial stability. The critical question is: can financial stability be ensured with declining profitability and solvency? Table 1 clearly signals about our banking sector that profitability has been falling, shortfall in provisioning is also on the increase ( fall in provisioning ratio) , and there has been a surge of 131 per cent in NPL in 2025 over the time span of just one year. Is it a sign of financial stability? We forget to realise that provisioning has a limit.

Our inherent weaknesses or failures lie in ignoring the need for removing the legal loopholes which the banks are facing practically and for tightening legal measures. We advocate for natural type of provisioning but strongly oppose massive or specific provisioning so that defaulters get little chance of escaping their fiduciary duties of loan repayments. Our loans are, as reported by Bangladesh Bank, mostly secured and as such, we should only look for ways and means to eliminate the legal hurdles to easy liquidation of securities held. The government should go ahead with stringency and uncompromising stance in the new socio-political environment to streamline credit management and to rebuild the economy. If we can, as part of good governance, disentangle banking business from undue political intervention based on national consensus and necessary legislation, bad loans would almost disappear and NPL would not go up beyond the normal level of discrepancy.

It is surprising to note that Basel Committee and national authority hardly assign maximum priority to stringent laws to recover defaulted loans. They stresses credit risk management by provisioning and recovering NPL through other means like seeking assistance from Asset Management Companies .Why does such an approach prevail? NPL ratio in Bangladesh is not only mounting (Table 2) but also the highest in Asia (Nonperforming Loans Watch in Asia 2025, ADB).The Bangladesh's industry sector ( manufacturing and service) alone accounts for more than 60 per cent of total NPL

(Table 2).

2020 -2024 , Bangladesh Bank

Basel's guideline requires banks to assess a loan's credit risk over its lifetime and recognises losses in three stages under ECL model . Stage 1: for performing loans (12-month ECL) ; Stage 2 : for loans with significant credit risk increase (lifetime ECL), and Stage 3: for impaired loans (lifetime ECL). This ECL approach, which aligns with IFRS 9, aims to provide a more accurate picture of a bank's financial health by provisioning for potential losses proactively.

Basel framework suggests for adequate allowance. When significant portion of total loans is NPL, then the question of adequacy in providing for loan loss becomes impossible. An acceptable level of credit loss is a very normal phenomenon, and for that purpose, we can support general provision like any non banking organisation's uncollectibles, not more than that. How far is it justifiable and feasible to make specific provisions ? Besides provisioning, some illogical exercises in the name of maintaining capital adequacy (purpose is commensurate with provisioning ) are observed in the banking practices. For example, risk-weighted assets of a bank are Tk.100. The bank is strictly instructed to provision 12.5 per cent for risk-weighted assets of Tk.100. It means the bank keeps a capital of only Tk.12.50 to cover up credit loss only Tk.12.5 while Tk 87.50 remains unsecured. How much risk is adjusted thus? This is not the right approach to handling credit risks. Specific provisioning means risking the bank, rewarding the defaulters and reducing owners' and employess' potential share of dividend and bonus.

We are in a process of improving banking governance. We should rethink about specific provisioning and take steps to reshuffle and bolster our loan recovery system to exit in phases from provisioning for classified loans. Integrated software for the banking industry encompassing the entire process of credit management including loan proposal making, loan processing and documentation, assessment of the real worth of securities, loan sanction, disbursement, spot supervision, monitoring income generation , recovery, communication, reporting and related issues. Stringent and unflawed recovery legislation is urgently required. A policy is imperative for appointment of branch-wise legal officers to exclusively deal with legal aspects of credit management and recovery. Would we be walking across that track?

Haradhan Sarker, PhD, is ex-Financial Analyst, Sonali Bank & retired Professor of Management.